Jul. 11, 2026 at 11:15 am GMT 2 min read

- The OCC approved Circle National Trust, a federally supervised trust bank for Circle’s digital-asset custody, not a full commercial bank.

- That structure could let Circle centralize custody and eventually attract institutional clients, strengthening its pitch around USDC infrastructure.

- Circle has not said when it will open, or whether reserve management and broader custody services will move in later.

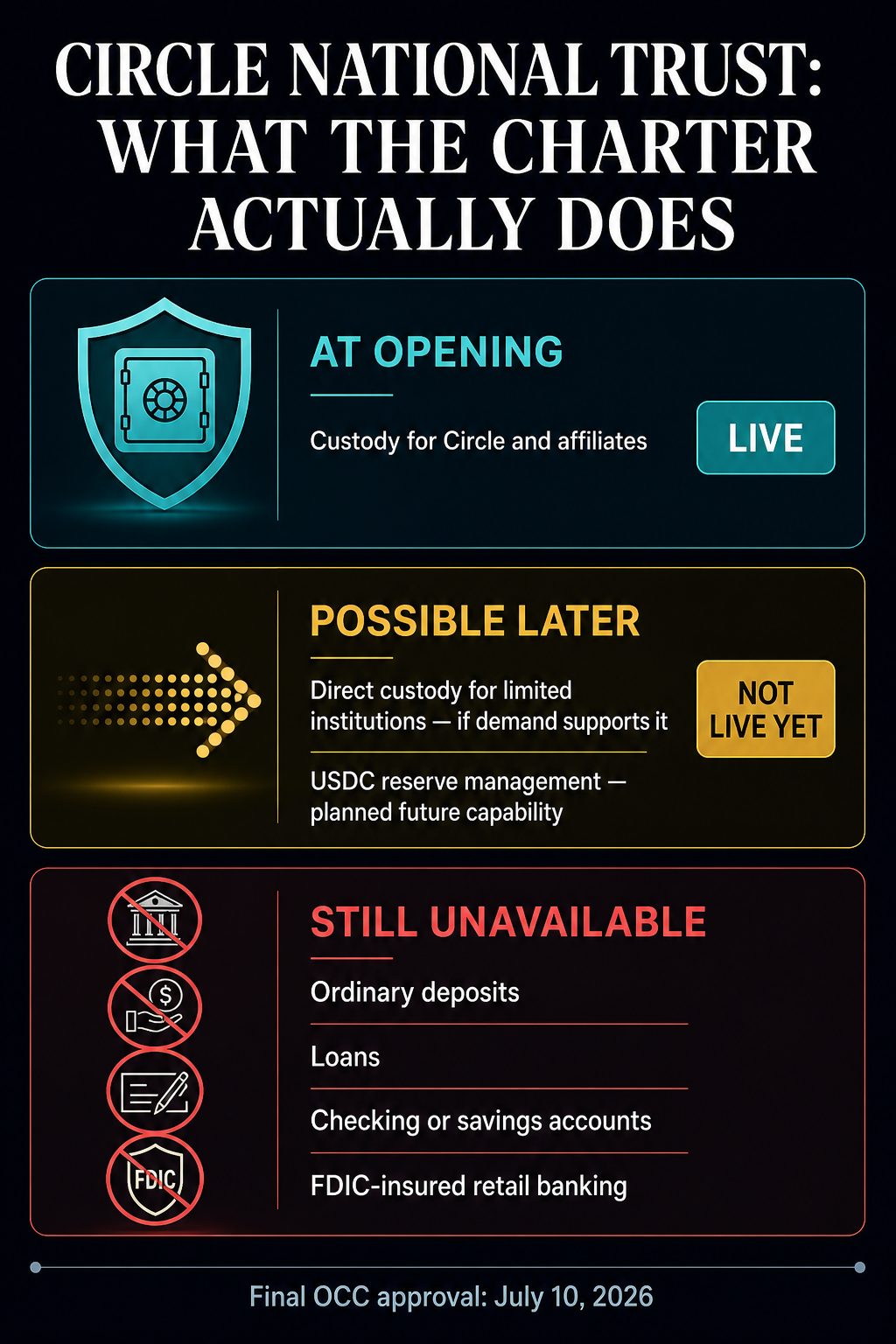

Circle received approval from the OCC on July 10 to establish a bank called Circle National Trust. That does not give the USDC issuer the powers most people associate with a commercial bank.

The national trust bank cannot accept ordinary deposits, make loans, offer checking or savings accounts, or provide FDIC-insured retail banking services. The decision is final, unlike the OCC’s preliminary conditional approval from December 2025, but its approved business remains centered on fiduciary custody.

What Circle can do at opening

Circle said the bank’s legal name will be First National Digital Currency Bank, N.A., operating as Circle National Trust. Upon opening, it will provide fiduciary digital-asset custody for Circle and its affiliates under direct OCC supervision.

That is the only service Circle has confirmed for the bank’s opening. Circle said the bank may eventually provide custody directly to a limited number of institutions, focusing on banks and other regulated financial organizations, if demand warrants expansion.

Managing the USDC reserve is also a future capability rather than a service that arrives with the charter. Circle has not disclosed when the bank will open or what additional operational steps must occur before reserve management moves inside it.

The charter’s strategic value lies in greater control over the infrastructure supporting a stablecoin with a market capitalization of about $73.3 billion.

A federal charter would let Circle bring custody, and possibly reserve management, under one roof instead of relying as heavily on outside firms. The company has not said what that might save or whether it plans to change its current partners.

The charter gives Circle a federal fiduciary framework that competing stablecoin issuers may find difficult to match quickly. That could help when banks and other regulated firms decide which digital-dollar infrastructure they are willing to use.

It does not automatically deepen USDC liquidity or place the token in more wallets, exchanges and payment products. Those distribution advantages remain contested as Open USD recruits major partners and challenges Circle’s issuer-led economics.

The charter also carries political friction. The Independent Community Bankers of America argued during the application process that national trust charters can provide nonbank fintechs with bank-like benefits without the full capital and consumer-protection framework that applies to insured commercial banks. The OCC nevertheless granted final approval.

The next tests are operational: when Circle National Trust opens, whether outside institutions demand its custody service, and whether USDC reserve management is later brought under the trust bank. Until then, Circle has gained federal supervision for custody—not the deposit-taking and lending powers implied by saying it simply “became a bank.”