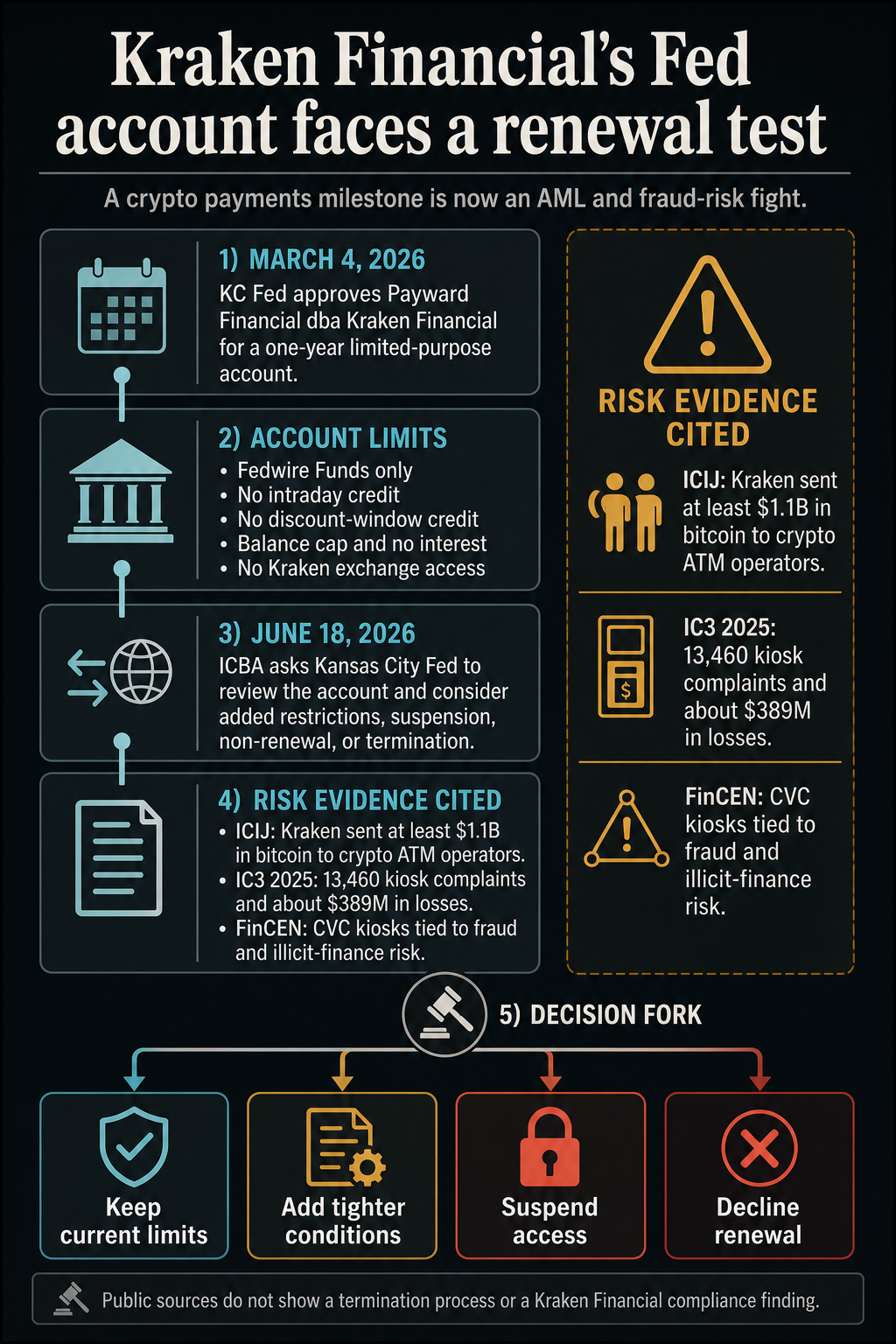

The banking group, ICBA, is asking the Federal Reserve Bank of Kansas City to turn Kraken's Fed account into an active renewal test before the initial one-year term expires.

In a June 18 letter, the community-bank trade group urged the Kansas City Fed to immediately review whether Kraken Financial's limited-purpose account remains consistent with the Fed's account-access guidelines and to consider further restrictions, suspension, non-renewal, or termination if warranted.

The request changes the tone around a limited-purpose Fed account that Kraken had framed in March as a direct-settlement milestone for crypto.

The Kansas City Fed approved Wyoming-based Payward Financial, dba Kraken Financial, for an initial one-year limited-purpose account under the Fed's Tier 3 review process.

Publicly described conditions grant Kraken Financial access to Fedwire Funds, excluding intraday credit, discount window credit, interest on balances, and use by the Kraken exchange or other subsidiaries within the Payward Group.

That combination makes ICBA's letter more than routine bank-lobby criticism. It creates a serious path toward tighter conditions or non-renewal because the account is already time-limited, risk-scored, and subject to restrictions.

The operative path is Kansas City Fed discretion over the account's conditions and renewal, with no automatic removal mechanism disclosed in the public record.

ICBA Wants a Kraken Fed Account Review Before Renewal

ICBA's core claim is that the existing account conditions do too little to address operational, legal, reputational, illicit-finance, and precedent-setting risks for a crypto-affiliated uninsured entity without consolidated federal supervision.

The letter asks the Kansas City Fed to scrutinize whether Kraken Financial's account remains consistent with the Fed's account-access guidelines and whether additional limits, suspension, non-renewal, or termination are warranted.

The practical target is in the renewal window. The Kansas City Fed approved the account for an initial one-year term, giving the Reserve Bank a defined point in time to reassess whether the experiment remains acceptable.

ICBA is trying to move that reassessment forward by linking the account to recent crypto-kiosk reporting and to the Fed Board's separate payment-account proposal.

The strongest version of ICBA's argument is procedural. The letter cannot force an outcome on its own, yet it provides the Kansas City Fed with a public record of objections from the banking sector before the first-year term expires.

For crypto firms, the stakes are direct access to settlement and reduced dependence on intermediary banks. For bank groups, the stakes are whether those rails open to firms outside the full bank supervisory perimeter without stronger off-ramps.

| Operational and legal risk for an uninsured crypto-affiliated entity | Tier 3 review and an initial one-year term |

| AML and fraud exposure tied to crypto-kiosk liquidity allegations | Ongoing risk assessment, added restrictions, suspension, or non-renewal |

| Precedent for other crypto firms seeking payment access | Reserve Bank discretion and the Fed Board's pending payment-account policy |

| Payment-system and credit exposure | Fedwire Funds-only service, no intraday credit, no discount-window credit, a balance limit, and no interest |

The Kansas City Fed's supplemental account notice is the main counterweight to ICBA's warning.

It frames the approval as Fedwire Funds access only, excluding intraday credit, discount-window credit, and interest on balances.

It also states that Kraken Financial is distinct from the Kraken exchange and other Payward Group subsidiaries, which have no access through the account.

Those details keep the approval from becoming a blank check for the broader Kraken business. They also show why the account is attractive to crypto firms.

Kraken described the March approval as a historic milestone that could provide it with direct payment infrastructure, improve Fedwire settlement, and reduce its reliance on intermediary banks.

CryptoSlate's March coverage treated Kraken's approval as a working example for stablecoin issuers and payments firms watching direct Fed access.

The June 18 letter tests that model from the other direction. A one-year, Fedwire-only account can be described as a controlled exception.

It can also be described as the first step toward broader access. ICBA wants the Kansas City Fed to treat the first description as binding and the second as a risk to be contained.

Kiosk Allegations Supply the Risk Evidence

ICBA's escalation draws its urgency from ICIJ's reporting that major crypto firms supplied bitcoin liquidity to crypto ATM operators while authorities were scrutinizing scam risks.

ICIJ reported that Kraken transferred at least $1.1 billion worth of Bitcoin to crypto ATM operators in recent years, including more than $700 million to Coinhub and at least $245 million to Byte Federal.

Kraken told ICIJ that it maintains robust compliance controls.

Those figures should be read as transaction-tracing claims, rather than adjudicated regulatory findings. They still give ICBA a way to connect the Kraken Fed account debate to crypto ATM fraud risk without treating the reporting as a finding against Kraken Financial.

The trade group is arguing that a limited-purpose account should be judged against the real-world risks posed by crypto liquidity flows, customer scams, and monitoring obligations related to suspicious activity.

Federal and state records make the kiosk concern easier to understand. The FBI's 2025 IC3 report showed 13,460 cryptocurrency ATM and kiosk complaints with about $389 million in losses, up 23% in complaints and 58% in losses from 2024.

Victims age 60 and older accounted for roughly $257.5 million of those losses. FinCEN's August 2025 notice linked convertible virtual currency kiosks to fraud, cybercrime, drug trafficking, and non-compliant operators that may mislead exchanges and depository institutions.

The state-level record remains mixed by legal posture. The DC attorney general alleged that 93% of Athena Bitcoin ATM deposits in the District during the relevant opening period were scam-related.

Missouri issued civil investigative demands to kiosk operators including Athena and Byte Federal. California said Coinhub must pay $675,000, including $105,000 in restitution, after kiosk-law violations.

Those actions address the kiosk ecosystem, not Kraken Financial's account compliance. They still explain why ICBA is treating kiosk liquidity as a Fed-rails issue.

If the Kansas City Fed views crypto liquidity relationships as relevant to account-access risk, the first-year review becomes a test of whether disclosed guardrails can absorb new fraud-risk evidence after approval.

The Kraken Fed Account Fight Meets the Fed’s Rulebook

The timing also helps ICBA. On May 20, the Fed Board requested comment on a payment-account proposal for legally eligible institutions that are not federally insured.

The proposal would preserve eligibility rules while adding standard terms, including no intraday credit, no discount-window access, no interest on balances, overdraft controls, and illicit-finance risk mitigation.

It also encouraged Reserve Banks to temporarily pause Tier 3 access decisions while policy work continues.

Governor Michael Barr dissented from that proposal, saying the safeguards were insufficiently specific and robust against money-laundering and terrorist-financing risks at institutions the Fed does not supervise.

He cited the absence of Fed examination and inspection provisions for AML and Bank Secrecy Act procedures.

That dissent gives the ICBA letter a regulatory echo inside the Fed's own policy process.

Alongside warnings that crypto firms may gain direct Fed payment access, the bank group is pressing the same unresolved issue that Barr flagged: how the Federal Reserve can control illicit-finance risk for institutions outside its consolidated supervisory reach.

Market prices are background to that policy fight. CryptoSlate's market pages put total crypto market capitalization around $2.17 trillion and BTC near $63,500 on June 22.

The dispute around Kraken Financial is small compared with that market scale, yet large as infrastructure precedent. A tightly conditioned Fedwire account can serve as a template for other crypto-facing firms to reference when seeking similar access.

The ICBA letter creates a serious path toward tighter restrictions or non-renewal, but that path runs through Kansas City Fed review and discretion.

The public record shows a pressure campaign, a limited account, an active Fed policy debate, and a set of fraud-risk allegations around the crypto ATM ecosystem.

No public source shows that the Kansas City Fed has opened a termination process or found Kraken Financial out of compliance.

That distinction will shape the next stage. If the Kansas City Fed leaves the account unchanged, Kraken Financial's approval becomes stronger evidence that limited-purpose accounts can withstand objections from the banking sector when controls are tailored to the applicant.

If the Reserve Bank adds conditions, suspends access, or declines renewal, direct Fed-rails access for crypto may stay case-by-case and constrained.

For now, the June 18 letter changes the story from an access milestone into a live supervisory test.

The next concrete signal is whether the Kansas City Fed responds publicly, asks Kraken Financial for additional information, changes the account limits, or lets the one-year term proceed toward renewal under the existing guardrails.