Ripple is trying to move the XRP Ledger (XRPL) deeper into institutional credit, a push that could expand the network’s role beyond cross-border payments and give XRP a broader claim on the next phase of onchain finance.

The company is backing a proposed lending upgrade that would allow institutions to borrow against assets they hold on the XRPL, including stablecoins and tokenized instruments, without forcing the blockchain to make the credit decision itself.

For XRP, the significance is less about turning the token into a lending asset overnight and more about widening the range of financial activity that can happen on the ledger where XRP is the native asset.

If the upgrade gains approval and adoption, XRPL would move further away from being judged mainly on payments activity and closer to a broader institutional infrastructure story.

XRPL lending enters crowded credit market

Ripple is trying to enter an onchain lending market already served by large DeFi protocols and private institutional networks, but its proposed XRP Ledger system takes a narrower approach than many of its rivals.

Over the years, Aave has shown that blockchain-based lending can attract large pools of capital. Private and permissioned systems have also gained traction with institutions that want tighter control over counterparties, compliance and risk.

XRPL’s proposed lending protocol is designed to sit between those models. It would keep the ledger public while allowing access to certain pools to be restricted through credentials when compliance rules require it. It would also embed the lending mechanics in the network’s core standards rather than leaving each application to design its own risk and repayment system.

The system is built around two proposed technical standards. XLS-65 would create Single Asset Vaults that pool a single asset on-chain. XLS-66 would provide the lending layer that allows those assets to be extended into fixed-term loans.

Both proposals still require approval from XRPL validators before they can go live on the main network. Ripple said developers and infrastructure providers can begin testing the features on a development network.

The design is intended to make loan execution predictable. A vault would hold a single asset. Approved borrowers would access liquidity from that pool under agreed terms. Once a loan is created, the ledger would enforce interest accrual, repayment schedules, and default procedures.

The main difference is where credit judgment takes place. In many decentralized lending markets, smart contracts, governance votes, and automated collateral rules shape the risk model.

Ripple’s proposal leaves underwriting, legal agreements, and compliance checks off-chain, while using the ledger to enforce what happens after lenders and borrowers agree to terms.

For context, a payment company holding RLUSD, Ripple’s US dollar-backed stablecoin, could use the system to bridge a short-term liquidity gap. If an expected cross-border settlement will not arrive for two days, the company could borrow from an approved pool to fund outgoing payments and repay the loan when settlement clears.

The same structure could be used by market makers financing inventory, treasury desks seeking short-term liquidity, or lenders building credit products around tokenized assets.

That approach could appeal to institutions that want clearer rules before committing capital. It could also make XRPL less flexible than more composable smart-contract networks, where developers can build and adjust lending products more quickly.

The trade-off reflects XRPL’s broader design history. The network has favored purpose-built functions over the open-ended smart-contract model used by Ethereum and other EVM networks. The lending proposal applies that same approach to credit.

Credit becomes the next test

Ripple’s timing reflects a broader shift in digital assets. Tokenization has advanced faster than the financing systems around it.

Treasuries, money market funds, stablecoins, private credit and commodities are increasingly represented on-chain. But once those assets exist on a blockchain, institutions still need ways to borrow against them, finance positions, manage liquidity gaps and allocate risk.

That is where Ripple is trying to position XRPL. The company has long marketed the network around settlement speed and payments. Lending would add another function: credit execution.

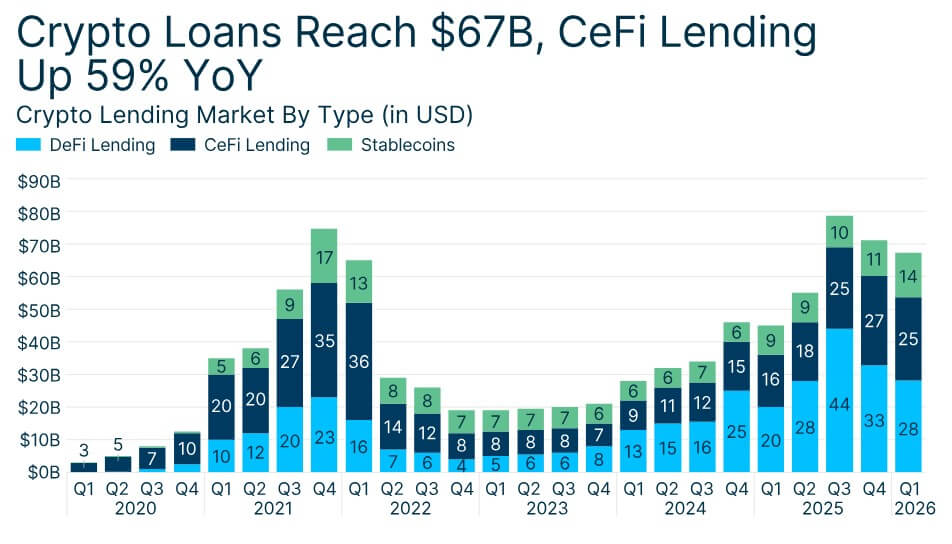

The opportunity is also tied to the recovery of crypto-backed lending after the failures of 2022. Silicon Valley Bank said loan volume across cryptocurrencies reached $67 billion in the first quarter of 2026, up nearly 50% from a year earlier.

Crypto Lending Sector (Source: Silicon Valley Bank)

Crypto Lending Sector (Source: Silicon Valley Bank)That rebound has come with a stronger focus on collateral, transparency and institutional risk controls. Ripple’s proposal aims to fit into that environment by providing institutions with an execution layer rather than asking them to rely entirely on crypto-native lending applications like Aave.

The design could also support Ripple’s stablecoin strategy. RLUSD has grown to about $1.56 billion in market capitalization since launching in late 2024, according to CryptoSlate's data.

If XRPL gains native credit markets, RLUSD could become one of the assets used in short-term liquidity facilities, especially for payment and treasury use cases.

That would not automatically translate into demand for XRP, because RLUSD and other issued assets can move on XRPL without XRP becoming the borrowed asset.

However, every new category of activity on the ledger strengthens the case for XRPL as a venue for institutional finance, and XRP remains the network’s native token used for fees and anti-spam protection.

Ripple’s larger question is whether that infrastructure can turn into sustained onchain volume.

Garlinghouse frames the gap

Ripple Chief Executive Officer Brad Garlinghouse recently said the company’s acquired businesses process about $16 trillion in annual payments and clearing activity, while digital assets account for close to zero percent of that volume.

That figure does not mean $16 trillion is ready to move through XRP. It includes traditional payments and clearing activity across businesses Ripple has acquired. But it shows the scale of the market Ripple is trying to convert.

Garlinghouse has framed that gap as an opportunity: to bring traditional finance onto blockchain rails using Ripple’s stablecoin, payments, custody, treasury, and prime brokerage infrastructure.

The lending proposal fits that strategy. Payments alone can move value. Credit can make those assets usable in financing, collateral and liquidity management. That represents a broader institutional pitch than the older XRP narrative, which focused heavily on cross-border settlement.

However, the market has not yet rewarded the shift. XRP is trading around $1.04 as of press time, down about 6% over the past week, according to CryptoSlate's data. The token has been pressured by the broader crypto downturn and remains far below its cycle highs.

That weakness makes the lending proposal more important for Ripple’s long-term growth trajectory. The company needs to show that XRPL can support institutional activity beyond speculative trading and payment corridors.

Security review clears major hurdle

The lending push follows a re-audit by blockchain security firm Halborn, which reviewed the protocol after significant code changes.

Halborn’s report, updated June 12, found five issues and no critical or high-severity vulnerabilities. The findings included one medium-risk issue, two low-risk issues, and two informational items.

Halborn said all reported findings had been addressed, though that category includes issues that were solved, acknowledged, or accepted as risk.

The most serious item involved a vault maximum-assets bypass through loan interest, which could have allowed a vault to exceed a configured exposure limit. Halborn marked that issue as solved.

The review also flagged edge cases around cascading defaults, vault freezes, grace periods, and cover-rate settings.

Those issues point to the main risk in the protocol’s design: the ledger can enforce agreed rules, but it cannot guarantee that the credit judgment behind a loan was sound.

That leaves investors and users with a clear distinction. The protocol can standardize execution. However, it does not remove borrower risk, administrator risk, or liquidity risk.

If a loan broker misjudges a borrower, vault participants can still lose money. If too much of a vault’s capital is locked in active loans, withdrawals could become difficult. If first-loss capital is too small, senior lenders may still face losses after a large default.

Those risks make the lending protocol more similar to traditional credit markets than retail DeFi yield products. Losses depend on underwriting, concentration, liquidity management, and legal recovery, not only on code.