Stablecoin supply climbed to a record $320 billion this week, extending the continued surge in dollar-linked digital assets.

This comes as one of the biggest questions hanging over the sector remains unresolved in Washington: whether the income generated by the reserves backing those tokens should stay with issuers or be shared with users.

Nonetheless, the new peak underlines how far stablecoins have moved from their original role as trading tools inside crypto markets.

Over the past year, dollar-pegged tokens have been increasingly used for payments, payroll, savings, and cross-border transfers, broadening their place in the financial system as lawmakers struggle to define the rules that will govern them.

That tension now sits at the center of the debate over the CLARITY Act, a broader bill on digital asset market structure that has become mired in the Senate over the treatment of stablecoin rewards.

A record market still runs through a few issuers and chains

The latest growth in the stablecoin market has been driven by the sector's biggest names.

Tether’s USDT now stands at $185 billion in market capitalization, up about $40 billion over the past year. It is followed by Circle’s USDC, whose supply has reached $78 billion.

This means that the two issuers are firmly in command of the stablecoin market’s core liquidity.

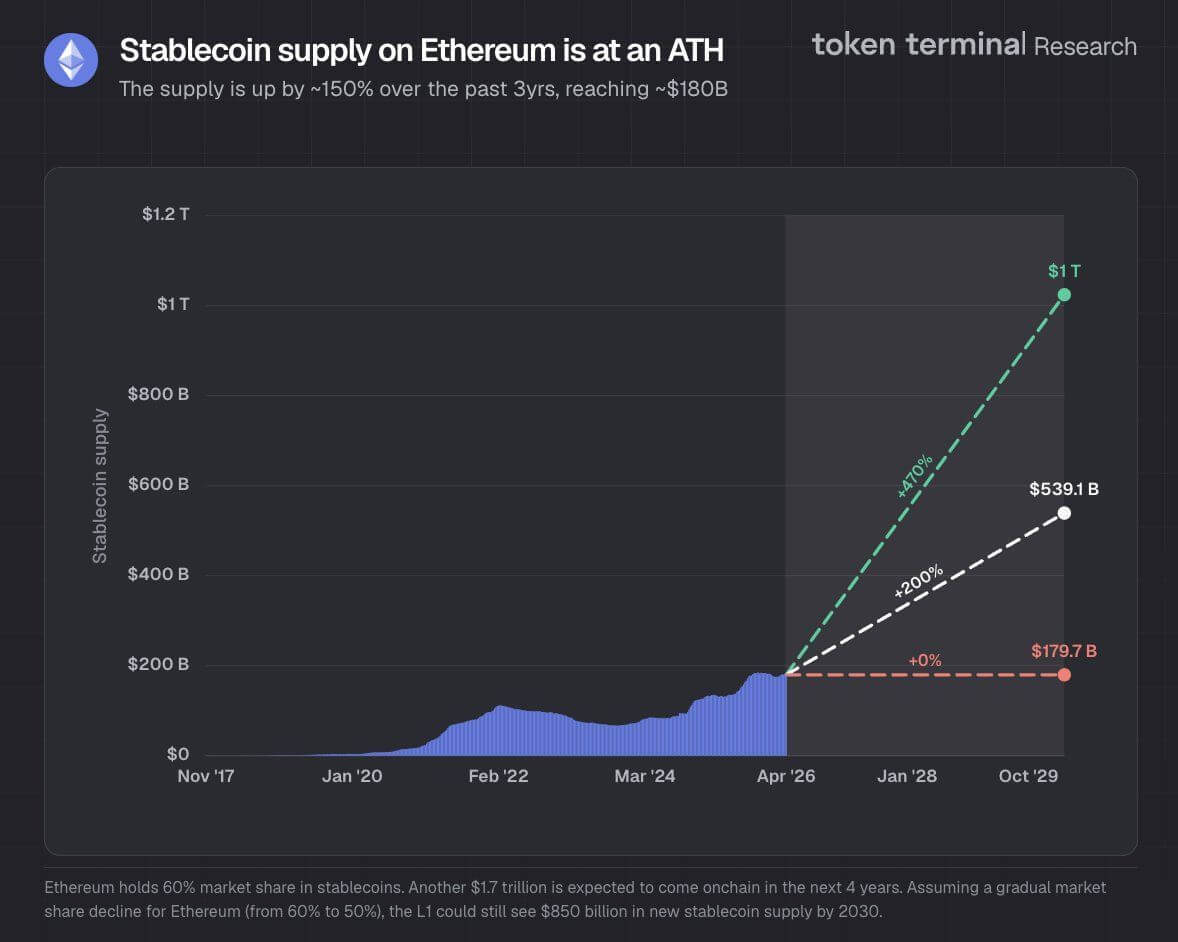

That concentration extends to the blockchains where those tokens circulate. Token Terminal data show stablecoin supply on Ethereum has risen about 150% over three years to roughly $180 billion, giving the network around 60% market share.

Stablecoin Supply on Ethereum (Source: Token Terminal)

Stablecoin Supply on Ethereum (Source: Token Terminal)Data from DefiLlama show that Tron ranks second with $86.958 billion in stablecoin, while Solana ranks third with $15.726 billion. Binance Smart Chain accounts for $13 billion, and Hyperliquid rounds out the top five with $5.229 billion.

Those figures show that stablecoins may be spreading into more parts of finance, but the market still depends on a narrow set of rails.

Ethereum remains the main home for tokenized dollar liquidity, especially where deeper pools of capital and broader decentralized finance activity matter. Tron continues to hold a major share of transfer-driven usage, helped by lower transaction costs.

Solana, Binance Smart Chain, and Hyperliquid remain smaller, but their presence in the top tier shows that stablecoin demand is broadening across networks designed for different user segments.

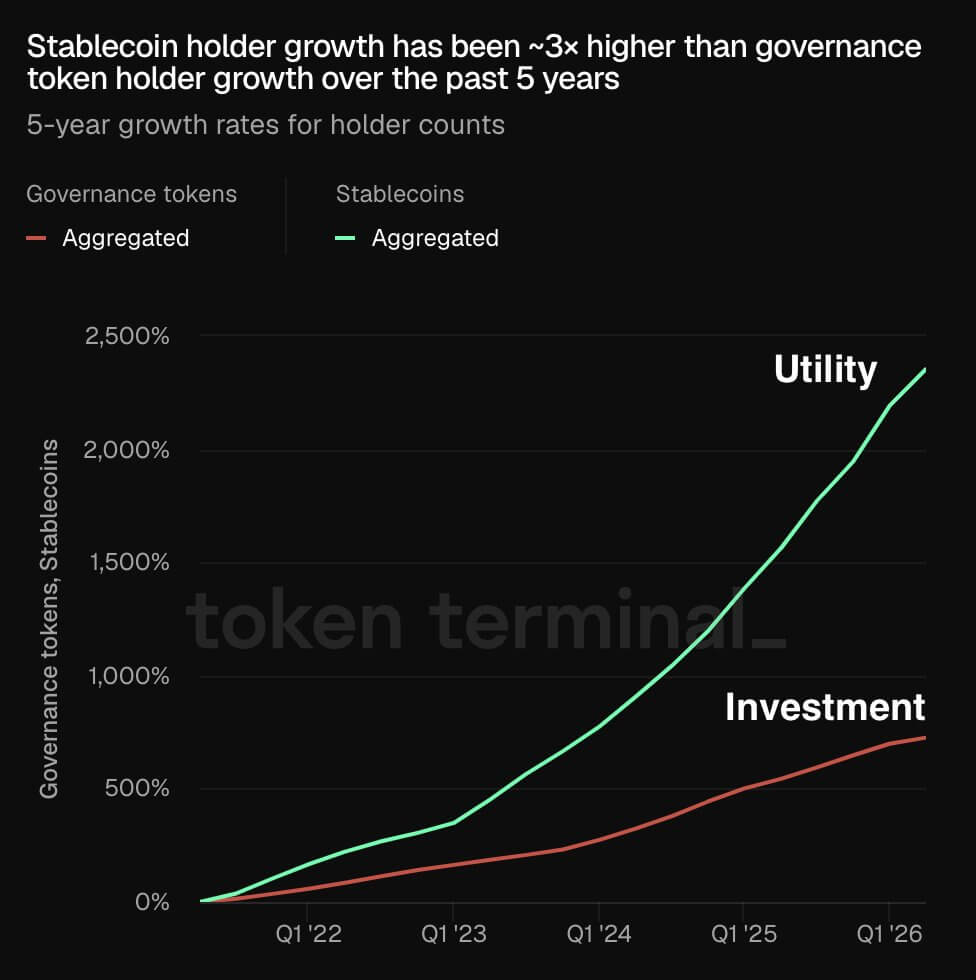

Meanwhile, the asset's holder base is also aggressively expanding. Token Terminal data show stablecoin holder growth has been roughly three times faster than governance token holder growth over the past five years.

Stablecoin Holders' Base (Source: Token Terminal)

Stablecoin Holders' Base (Source: Token Terminal)That divergence suggests users are moving toward blockchain-based dollars with direct utility rather than tokens whose value depends more heavily on protocol participation or speculative positioning.

That shift helps explain why stablecoins have continued to grow even when other parts of the crypto market have moved in and out of favor. The more they behave like financial infrastructure, the less dependent they become on pure trading momentum.

Stablecoins move into savings, payroll, and payments

That utility case is becoming clearer in consumer and business behavior.

The Stablecoin Utility Report 2026, produced by BVNK in partnership with Coinbase and Artemis, found that stablecoins are increasingly used in everyday financial activity rather than solely as trading collateral.

The report notes that users are allocating a growing share of their income and savings to dollar-pegged tokens, reflecting a shift in how those assets are viewed across markets.

Businesses are also adopting these instruments more quickly for practical use. The report found that 77% of surveyed firms use USDC, signaling that stablecoins are becoming embedded in business-to-business settlement and treasury activity, not just exchange flows.

Meanwhile, the same pattern is visible in transaction data. Ripple noted that fintechs and financial institutions have led the latest wave of stablecoin adoption, with global annual transaction volumes rising to $33 trillion last year.

Stablecoins now account for 30% of all on-chain transaction volume, a figure that reflects their central role in the broader blockchain economy.

Notably, the strongest demand is emerging where dollar access and currency stability matter most. Stablecoin adoption is rising in countries facing inflation and exchange-rate pressure, including Nigeria, where dollar-pegged tokens are actively used to preserve value and manage currency depreciation.

In those markets, stablecoins function as a savings tool, settlement rail, and payment instrument simultaneously.

As a result, industry projections show that daily stablecoin transaction volumes could reach $250 billion by 2028, while the asset supply could reach nearly $4 trillion by the end of the decade.

Whether that level is reached on schedule or not, the trend is already established.

Stablecoins are expanding because they solve specific problems that make cross-border transfers faster, dollar access easier, and value easier to store in a unit that users trust more than local currencies.

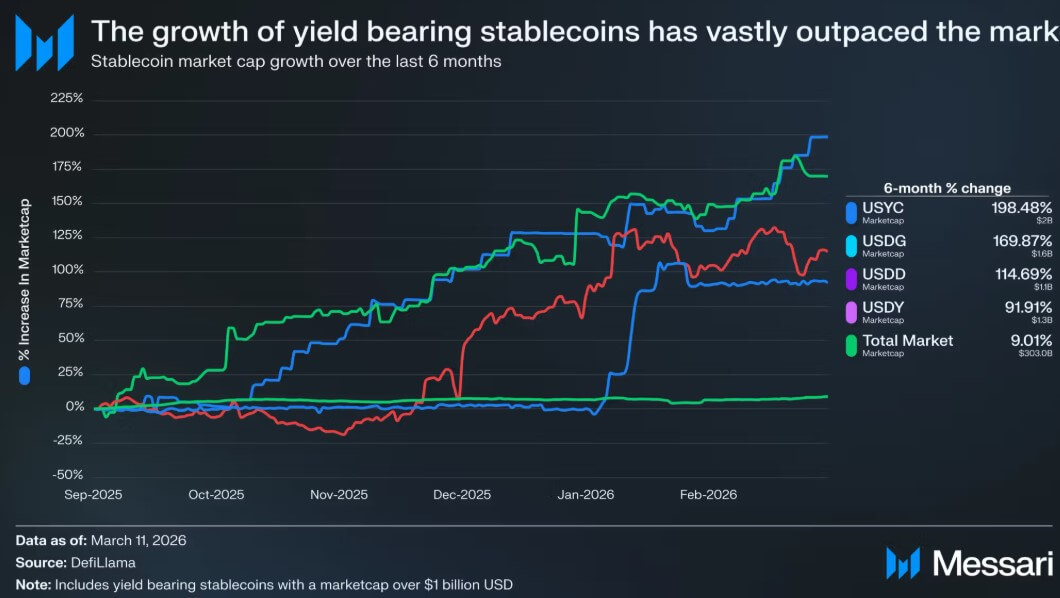

Yield-bearing stablecoins are growing faster than the rest of the market

However, the market is already showing that crypto users are increasingly demanding yield on using or holding their dollar-pegged assets.

Yield-bearing stablecoins, which generate returns for holders through structures tied to tokenized Treasuries, DeFi lending, or derivatives, have begun to pull away from the broader stablecoin market.

Messari data show that over the last six months, growth in yield-bearing stablecoin supply has outpaced the broader stablecoin market by more than 15 times, with the divergence beginning around mid-October 2025.

Yield-bearing Stablecoins (Source: Messari)

Yield-bearing Stablecoins (Source: Messari)That gap is telling. It suggests users are not satisfied with simply holding digital dollars that preserve nominal value. They increasingly want idle on-chain cash to produce income.

In some products that happens through auto-accruing designs. In others, it happens through staked variants such as sUSDe. The structures differ, but the underlying demand is the same.

The firm pointed out that the leading issuers in that segment also reveal something about where the market may be heading.

According to Messari, the biggest winners in yield-bearing stablecoins are not primarily payments companies. They tend to offer a single yield-focused asset, operating more like tokenized money market funds or deposit substitutes than like payment networks.

In other words, the market is already splitting into two lanes: transferable dollar tokens built for movement and yield-focused dollar tokens built for return.

That is the split now haunting the CLARITY Act. If payment stablecoins remain barred from sharing reserve income while yield-bearing alternatives continue to grow, lawmakers will not be deciding whether this market exists, but which version of these assets wins.

The Senate’s delay is turning the policy fight into a deadline story

That decision is becoming more urgent as the political calendar tightens.

The CLARITY Act passed the House in July 2025 but remains stuck in the Senate as lobbying intensifies over stablecoin rewards. The GENIUS Act bans issuers from paying interest directly to holders, but it does not prohibit third-party platforms, such as exchanges, from offering yield.

That has turned stablecoin rewards into the most contentious unresolved issue in the wider push for digital asset legislation.

Banks argue that allowing such stablecoin rewards would disrupt the traditional funding model.

The American Bankers Association has warned that if stablecoins become easily accessible, yield-bearing assets, and deposits could flow out of the banking system, especially from smaller regional and community lenders.

Those institutions would then have to replace low-cost deposit funding with more expensive wholesale borrowing, squeezing net interest margins and potentially reducing credit availability.

Crypto firms like Coinbase argue the opposite. They say banning rewards would suppress innovation and preserve an uneven financial system in which stablecoin issuers collect income from reserves while users receive nothing.

They also argue that banks themselves could participate in the opportunity rather than merely defend against it.

As a result, the White House has convened several meetings since the beginning of the year to break the stalemate, but no compromise has emerged.

That has increased concern that the bill is running out of time in the legislative window. Senate Banking Committee Chair Tim Scott has yet to schedule a markup date, though supporters, including Sen. Bill Hagerty, have said they hope the committee can move the legislation before the end of April.

However, the procedural timetable leaves little margin for delay.

Justin Slaughter, vice president of Paradigm affairs, said the mechanics of a Senate floor vote generally require two to three weeks, meaning the bill would need to clear the banking committee by mid-May to reach a vote before Memorial Day.

If it slips past that point, the calendar becomes more hostile, with long non-legislative periods from Aug. 10 to Sept. 11 and again from Oct. 5 through the Nov. 3 election.

Even the text aimed at resolving the fight is slipping. Sen. Thom Tillis said the latest draft language on stablecoin yield would likely not be released this week because he wants clarity on the timing of the Banking Committee markup.

Tillis has been working with Sen. Angela Alsobrooks on a proposal designed to settle the dispute over whether crypto companies should be allowed to pay interest on idle stablecoin balances.

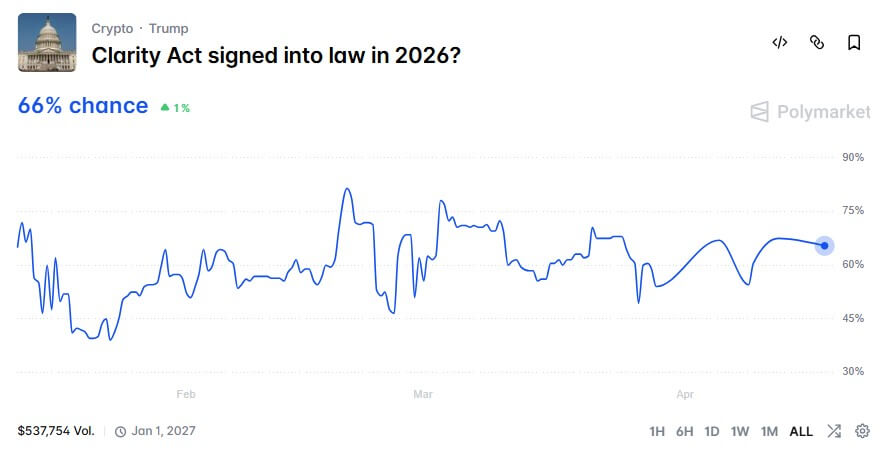

Markets are already reflecting that uncertainty. Polymarket data put the odds of the bill passing at 66%, down from more than 82% in February.

CLARITY Act Odds of Passage in 2026 (Source: Polymarket)

CLARITY Act Odds of Passage in 2026 (Source: Polymarket)Stablecoin supply, meanwhile, has continued to climb.

That is what gives the current moment its shape as the market is setting new records. Stablecoins are becoming more deeply embedded in payments, savings, and business transfers. Yield-bearing alternatives are outperforming the broader sector.

Yet the most important economic question inside that expansion remains unresolved in Washington.

Patrick Witt, executive director of the President’s Council of Advisers for Digital Assets, said the dominant players across crypto remain foreign, from stablecoin issuers to centralized exchanges and DeFi protocols, and warned that without a durable market structure framework, the United States will continue to fall behind in digital assets.

For now, the market is not waiting. Tokenized dollars are scaling first, while Congress is still arguing over who should be allowed to benefit from them.